Last weekend, Laughlin Law Firm spent some time in the sun and on the water with some of Des Moines' finest real estate professionals.

Here are some pictures from the event!

Viewing entries tagged

Real Estate

Last weekend, Laughlin Law Firm spent some time in the sun and on the water with some of Des Moines' finest real estate professionals.

Here are some pictures from the event!

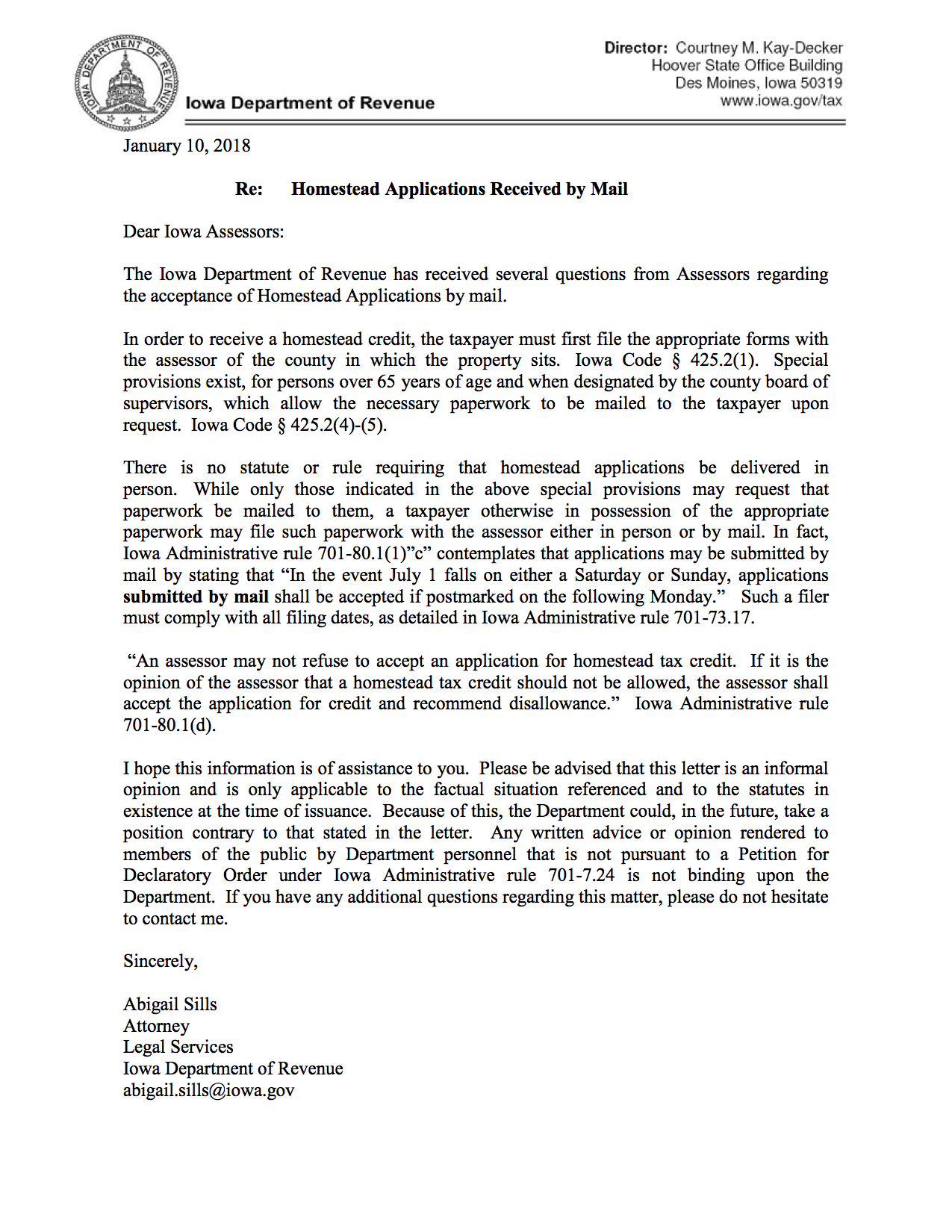

Those of you who are avid followers of the Laughlin Law Firm blog (which we know all of you are!) will have noticed that we recently began looking into what counties in the mid-Iowa region are equipped to allow homeowners to apply for their Homestead Tax Credit applications online.

In doing so, we discovered that certain county sites published a requirement that a person must file their application in person. That prohibition seemed off, so we did some extra digging into the Iowa Code and the Iowa Administrative Code. Then, we inquired with the Iowa Department of Revenue and posited that such policies were invalid and inconsistent with state and administrative law. The Department said they would look into it and get back to us.

Sure enough, they did and they agreed. Not only that, they have since taken the initiative to notify all assessors’ offices that they are required to allow both personal and mailed forms of the application! The letter below was their notice to the assessors.

Meanwhile: Here is a link to the uniform Homestead Tax Credit application

We invite you to put it in your closing binder packet to better reflect your services to your clients. Better still, you can rely on us to bring it to the close since we now include that information in our closings.

Either way, now you can confidently advise your clients of their Homestead Tax Credit Application mailing rights and give them one more reason to leave the closing table impressed with you and your services.

Another successful DMAAR Annual Event in the books! Here's a photo of just some of our talented real estate friends with our team members. We truly value our relationship with DMAAR, and our hats are off to all of the award participants, nominees and winners from Friday. We can't wait for next year!

Congratulations to all the 2017 Volume Winners (Individuals who sold over $10.7 million in 2017), all Unit Award Winners (Individuals closing 50 or more units), and Rookie Volume Winners (Individuals in their first consecutive 12 months of selling who sold a volume of sales over $7.5 million)

Here are some pictures from Laughlin Law Firm's experience at the fantastic event (click photo to view all):

While scarfing down a quick hot lunch on a ridiculously cold Iowa day (below zero at the time of writing), I came across the following article on CNN.com: http://money.cnn.com/2017/12/26/pf/prepay-property-tax/index.html.

It appears that in high-dollar property tax states, homeowners are lining up to prepay their property taxes by year end in order to avoid the $10,000 deduction cap recently adopted pursuant to The Tax Cuts and Jobs Act, now efficiently renamed to comport with parliamentary procedure as the "To provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018" Act (it’d be hard to make this stuff up).

While prepayment may seem attractive, and assuming you have thousands of dollars laying around after the holiday buying season, take a few moments to consider whether this action will yield result you desire. For instance:

1. Is this really the most effective use of your dollars, even assuming you’ll realize the deduction? Might that money be more effectively utilized in some other higher-yielding investment with a more certain return?

2. Will your county allow for prepayment? And if not, will you be able to effectively petition for a county policy revision in time to realize the gain?

3. What will the IRS have to say about this action? I’m betting a lot. Bear in mind that the IRS has not weighed in with guidelines and regulations governing implementation of the bill. Will a payment made in 2017 for taxes upon the homestead applicable for the fiscal year 2018 be deductible irrespective of when made? If you’re in a state like Iowa where property taxes are paid “in arrears,” what will be the effect of that retroactive annual taxation? Will it bode more favorably (i.e. a 2nd half property tax installment payment due in March of 2018 is actually applied to taxes imposed upon the property for the period of January through June of 2017)? Will that cap be imposed upon 1st half property tax payments due in September of 2018 for the tax period of July through December of 2017? Those are really big “if’s”. Be aware that most, if not all counties, will decline to estimate taxes and/or accept tax payments that are not yet “certified”.

4. If you do take the plunge, you’ll want to be doubly sure that your payment will be effective in the current fiscal year. Each county in Iowa, for instance, has some discretion as to how they accept payment, and as to how they credit payment. So, as the article astutely points out, you’ll want to ensure you get the check there appropriately.

5. Do you itemize your deductions? If not, then you won’t be able to deduct state and local taxes anyway. There are also some considerations to be made for those subject to the Alternative Minimum Tax. Have you spoken with your CPA? It would be wise.

6. Do you have an escrow account as a condition of your mortgage? Have you contacted your lender about your prepayment plans? Lenders, under federally-backed mortgage loans, have strict rules for handling escrow funds and for dealing with excess taxes and insurance (an excess being created by your prepayment). Furthermore, you’ll want to ensure that the rate of tax collection for purposes of escrow in 2018 is adjusted for the prepayment. Overpaying into escrow is likely not a wise strategy.

According to SmartAsset.com, the State of Iowa has an average effective property tax rate of 1.44%, ranking it as the 14th highest rate in the country. So, if Zillo is correct, and the median home listing value in Iowa stands at $169,000, that amounts to a tax bill of about $2,500 - well below the $10,000 federal cap. Perhaps it’s much ado about nothing (unless of course, your house is worth in excess of $700,000). So if you have money to burn, tread lightly, and if you don’t, it may not be best to tread at all.

**Please keep in mind that I am not YOUR attorney, and that the above is not intended as legal advice for your individual circumstances. Seek out a qualified attorney and accountant or CPA for proper advice on the foregoing.

As is typical with the passing of any July 1st, the Iowa Code tends to get a makeover. These changes can go unnoticed, or they can be total game changers. Naturally, all of that depends upon where your interests lie.

One significant change may not have made many headlines, but it has certainly grabbed the attention of the state’s developers, contractors, insurers, attorneys, and buyers in the commercial and residential markets alike. This was the amendment to the statute-of-repose period set forth in Iowa Code §614.1.

Iowa Code §614.1 was amended to reduce the statute-of-repose period for any real property improvement project that begins after July 1, 2017. This limits the window for bringing suit against a real property contractor if that contractor’s work negligently results in an unsafe or defective condition to the property. The previous statutory period for bringing suit was 15 years for single-family and two-family residential dwellings. That period has been reduced to ten years. Additionally, most other structures, including larger residential dwellings and commercial buildings, have seen this window reduced from 15 years to eight years.

In recognizing the application of this changeover, one must first distinguish between a Statute-Of-Repose (SOR) and its more widely recognized cousin, a Statute-Of-Limitations (SOL). Both are time constraints that limit the time period in which a person is allowed to bring a lawsuit against another party. The key difference between the SOR and SOL is when the clock starts ticking. The SOL begins running on the date a party is injured or discovers their injury. This date otherwise is known as the event that gives rise to a cause of action. An SOL applies in instances of physical injury and in many criminal matters. By contrast, a SOR begins running the moment a specific event occurs, namely the completion of a construction project or property improvement.

How significant is this change? Well, if you ever find yourself on the plaintiff’s side or the defendant’s side of pending litigation, the very first thing either attorney checks is whether or not the statutory period to bring suit has expired. Someone who would otherwise have a perfectly good legal claim against someone else is going to be barred from bringing their lawsuit once the expiration date on that time restriction passes. In that sense, it is quite literally a deal maker or deal breaker.

Hence, the smaller the window someone has to sue over their claim, the less likely a possible defendant is going to get tied up in costly litigation and the more likely a possible plaintiff will need to recognize their position and plan accordingly. As always, it comes back to perspective.

The benefits and risks of this change are best met with a thorough assessment of your position in these hierarchies and how the more nuanced factors of this law relate to that perspective. Chances are this shift directly affects your business, your contractors, your sub-contractors, your insurance costs, and it might be as intimate as how it affects the very place you call home.

We invite you to plan accordingly.

===

https://www.legis.iowa.gov/legislation/BillBook?ga=87&ba=sf413

https://www.legis.iowa.gov/docs/code/614.pdf

https://www.legis.iowa.gov/docs/publications/SOL/860352.pdf#SF413

(SF 413, pgs 60-61)

SENATE FILE 413 – Improvements to Real Property – Unsafe or Defective Conditions – Limitations on Actions BY COMMITTEE ON JUDICIARY. This Act reduces the statute-of-repose period in cases arising out of the unsafe or defective condition of an improvement to real property for certain types of property. A statute-or-repose period differs from a statute-of-limitations period in that a statute of repose establishes a time period after which a lawsuit cannot be filed regardless of whether an injury has occurred. A statute-of-limitations period begins at the date of the injury or upon discovery of the deficiency.

Under prior law, a case arising out of the unsafe or defective condition of an improvement to real property was subject to a 15-year statute of repose. The Act provides that for actions arising out of a nuclear power plant or interstate pipeline, the period remains 15 years. For actions arising out of the construction on single-family or two-family dwellings occupied or used primarily for residential purposes, the period is reduced to 10 years. For actions arising out of any other kind of improvement to real property, the period is reduced to eight years. However, for actions arising out of intentional misconduct or fraudulent concealment, the period for the statute of repose is 15 years, regardless of the type of real property. If the unsafe or defective condition is discovered within the final year prior to the expiration of the applicable period of repose, the period is extended for an additional year.

The Act does not reduce the statute of repose for real property improvements in existence prior to July 1, 2017, or to improvements to real property, whether construction has begun or not, that are the subject of a binding agreement as of July 1, 2017.

====